Digital banking

Third time lucky

Banks that have no branches are making a surprising resurgence

Nov 9th 2013 | PARIS |From the print edition

BEHIND the smoked glass of a nondescript building in central Paris young people in open-necked shirts interact with Twitter and other social-media networks. This has the feel of a start-up, but in fact it is an outpost of BNP Paribas, one of France’s biggest banks. Hello Bank!, with its catchy name and irritating punctuation, represents one of the most voguish trends in banking. It is trying to entice customers to abandon expensive bank branches and do most if not all of their banking on their mobile phones and tablets.

Hello is far from alone in trying to wean customers from bank branches. Newly minted online banks include Simple and Moven in America, Holvi in Finland and Rocketbank in Russia. All this may seem wearily familiar. Around the time of the internet bubble in 2000, new online banks such as Wingspan in America and Egg in Britain launched with a promise to reinvent banking. Most of them soon closed or were sold, defeated by clunky technology and the conservatism of customers.

A second wave of digital banks took off in the mid-2000s, with more modest ambitions. Instead of seeking to entice customers away from their existing banks, they merely tried to poach a share of their savings. Firms such as ING Direct and Icesave attracted deposits by offering little more than mouthwatering interest rates. But the savings they achieved by eschewing bricks and mortar were not enough to pay for such enticing offerings; they also had to invest in high-risk assets that blew up during the financial crisis.

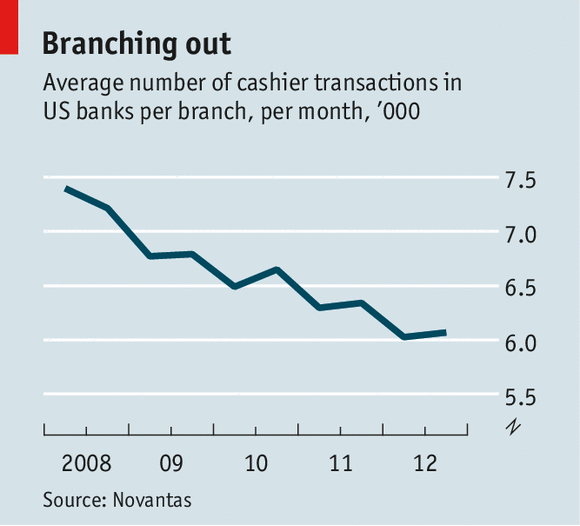

Technological advances make the third wave of digital banks look more sustainable. The proliferation and sophistication of smartphones and tablets allow banks to offer many more services online. Instead of having to choose between queuing in a branch or sitting down in front of a computer, customers can now check balances or pay bills using their phones while sitting on the bus. They can deposit cheques by photographing them and accept credit-card payments using their phones. As a result, the number of transactions taking place in branches is falling steadily (see chart).

Joining online banks is much easier these days too. In markets where regulators allow it, Hello lets customers open new accounts entirely online, using smartphones to take photographs of their identity documents and utility bills.

New online banks are also able to offer customers things the old ones couldn’t. For example, Simple has a clever search box that enables customers to type in queries such as “How much did I spend on taxis in New York last month?” or “How much have I spent on coffee this week?” Holvi has built its bank around an accounting system that lets groups of friends or workers at small firms manage budgets and allocate funds to projects. Making payments and safeguarding cash, the essence of banking, happen almost as an afterthought in the background.

Customers’ perceptions of the safety of online banking are also improving. Surveys show that 18- to 29-year-olds in America choose their banks mainly on the basis of their online offerings. Proximity to branches, the main criterion for people in their 70s, barely features, says Sherief Meleis of Novantas, a consulting firm.

To be sure, established banks are also being pushed into doing more online. Low interest rates in most of the rich world are crushing the profitability of retail banking by compressing the difference between the rates banks earn on loans and the very low rates they offer to depositors.

Reducing the number of branches offers the potential for huge savings, since these account for about half of all costs in retail banking. Yet the dilemma facing banks, new and old, is that the most complex and profitable financial products, such as mortgages, are still sold in branches. It also tends to be easier to entice customers to use several such products in person.

In moving to an online-only model, banks risk losing their most profitable clients while gaining the ones who are most promiscuous in their relationships with banks, reckons Andy Maguire of BCG, a consulting firm. Until online banks become better than the traditional sort at selling things like mortgages and getting their customers to make use of multiple offerings, they are likely to remain exciting experiments that appeal to the young and technologically adept. If they get it right, however, the threat to the bricks-and-mortar banks will be serious.

No comments:

Post a Comment